Wealth Matters: Earth Day by Mutual Trust

The world is facing the twin challenges of energy security and sustainable generation. Global energy demand is projected to rise by around 50% by 2050, driven by population growth, industrialisation and electrification. While clean energy investment has surged, over US$1 trillion committed since 2020, traditional energy sources remain vital, with natural gas expected to grow as it replaces coal.

This article by Wigmore member firm, Mutual Trust, published in recognition of Earth Day 2025 under the theme “Our Power, Our Planet”, explores how strategic investment and innovation across the energy supply chain are shaping the future. It highlights opportunities for investors in companies transitioning to lower-emission solutions, businesses enabling the energy transition through critical minerals and storage technologies, and leaders pioneering new approaches to energy production.

From carbon capture initiatives by major oil and gas producers, to breakthroughs in thermal storage and solar technology, the piece underscores the importance of a diversified approach to energy investment. As the article notes, “Energy security is not just about keeping the lights on; it’s about ensuring economic stability and national security.”

Click below to read Mutual Trust’s article in full by downloading the PDF.

Turim, a Certified B Corporation: A milestone in their journey

Turim, a Wigmore Association member firm, is proud to announce that it has been officially certified as a B Corporation. This certification is a significant milestone in their journey, reinforcing their commitment to their clients, employees, and the global community.

As a B Corp, Turim is recognised as a company that seeks excellence in its services, while also taking an innovative and sustainable approach to its business. This certification reflects their ongoing promise to place collective benefit at the centre of their operations, guided by strong principles of responsible governance.

Chief Sustainability Officer Roberta Goulart said, “By becoming a B Corp, we join the ranks of the 300 Brazilian companies leading this global movement, reinforcing our commitment to these core values. We continue to preserve our culture, the quality of our service, and guide our clients innovatively to collectively make a positive impact on the world.”

The B Corp certification is a rigorous process that evaluates a company’s performance in areas such as environmental sustainability, social responsibility, and corporate governance. Turim is proud to have achieved this certification, which is a testament to their commitment to making a positive impact on the world.

Turim is dedicated to providing their clients with the highest quality of service, while also striving to make a positive impact on the world. This certification is a reflection of their commitment to these core values, and they are proud to be part of the global B Corp movement.

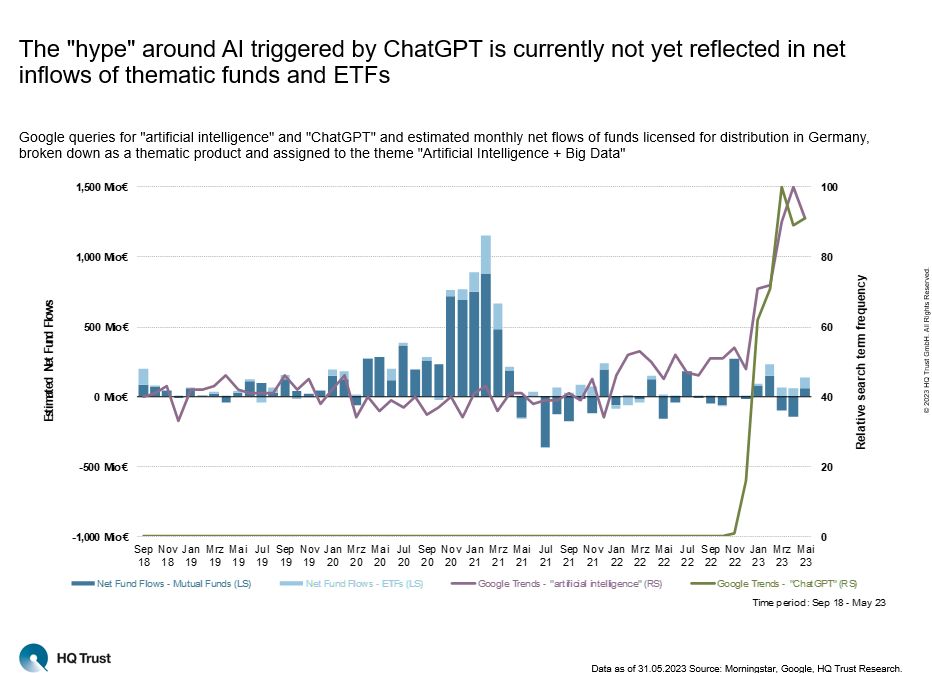

The AI Hype Leaves Fund Investors Cold

On the stock market, two letters have recently caused great euphoria: AI. The launch of ChatGPT has given a huge boost to interest in artificial intelligence. After the company OpenAI presented its chatbot in November 2022, demand for Google and some other tech stocks virtually exploded. Jan Tachtler investigated whether the same is true for AI funds and ETFs.

The capital market analyst at HQ Trust and co-portfolio manager of HQT Megatrends evaluated the search queries on Google for the topics "artificial intelligence" and "ChatGPT" and contrasted them with the estimated monthly net flows of all funds and ETFs licensed for distribution in Germany. These funds were categorized by Morningstar as thematic products and assigned to the topic "Artificial Intelligence + Big Data". Currently, a total of around EUR 12 billion is invested in these products. The analysis covers the period from September 2018, when the first ETF was launched, to May 2023.

- "The 'hype' around AI, triggered by ChatGPT, is currently not yet reflected in net inflows into thematic funds and ETFs."

- "Since November 2022, the estimated net inflow for AI funds and ETFs is €335 million. This is just 2.9% of the capital currently invested in this area."

- "In 3 of the past 7 months, outflows were actually higher than net inflows for these products."

- "Most recently, it has been the ETFs that have benefited from net inflows. However, they are still far from the high points of 2020 and 2021."

- "Inflows into AI funds and ETFs were highest in February 2021, at around €1.2 billion. By comparison, these products saw inflows of just €140 million in May 2023.

Lessons learned from the present Inflation episode

No one could have predicted the inflation effects of covid pandemic and the Ukraine war with any accuracy. But the European central bank's misjudgements were particularly pronounced and consequential. The fight against unexpectedly high inflation will weaken growth and burden households and firms. These costs cannot be avoided. However, they can be limited if the central bank pursues a clear and reliable stabilization course.

The current debate on the ECB's monetary policy mainly revolves around the question how many more interest rate hikes could be in store before the peak in this cycle is reached. Most financial markets expect two (smaller) rate hikes by the end of the year. However, there could be more if core inflation, which is not directly influenced by energy and food prices, remains as stubborn as it has been in recent months. For bond markets and stock prices, the policy stance is certainly of high relevance, and may cause recovery or setbacks.

From a long-term perspective, the important question is, what conclusions the ECB may draw from the experience of the past decade and a half, in which inflation targets were first clearly undershot despite ultra-expansive policies, and then exceeded them in a rather drastic and unexpected manner from 2021 onward, forcing the ECB into an abrupt turn-around. What are the "lessons learned" from this development?

In times of low inflation, the ECB changed its strategy in 2021

As a starting point one needs to look at the strategy review that the ECB completed in July 2021. Under the impression of years of low inflation and a downward trend of real interest rates, the ECB announced some changes. Most importantly, a symmetric and medium-term inflation target of 2% was set, replacing the previously applicable stability target of below, but close to 2%, inflation. Also, the ECB confirmed the potential use of unconventional instruments such as longer-term interest rate guidance ("forward guidance"), large-scale bond purchases, long-term loans, and negative key interest rates.

Regarding the analytical framework for monetary policy decisions, the Bank announced an integrated approach replacing the previous two-pillar system with an economic and a monetary pillar. With this change the relevance of monetary aggregates for policy decisions is qualified further. The integrated analytical framework also allows greater attention to be paid to the real economic and financial consequences of ECB policy. The strategy is complemented by stronger support for climate targets.

Serious Misjudgments of Inflation

Neither central banks nor other forecasters have complete foresight about future economic and price developments. The consequences of sudden shocks, such as the Covid pandemic and the energy crisis following Russia's attack on Ukraine, cannot be predicted with any precision. Their impact on inflation was significant. On the one hand, demand for goods rose strongly in 2020 and 2021, while production was depressed by supply constraints and disrupted supply chains. Energy price shocks came on top.

Few forecasters caught these effects early. However, the central bank's misjudgments were particularly pronounced and of high relevance for the stance of monetary policy. Ciiting the transitory nature of inflation and favorable projections for price stability, the ECB was slow to change its policy. Even in November 2021, when the annual change in the Harmonized Index of Consumer Prices had reached 4.9 percent, ECB Director Isabel Schnabel like other ECB representatives argued, "We expect inflation to have peaked in November [21] and for inflation to decline gradually again in the coming year, towards our inflation target of two percent."

Things turned out completely differently - admittedly also because of the Ukraine war. In the spring of 2022, the ECB then signaled a stronger need for action, but it wasn't until July 2022 - with inflation at a whopping 8.9% - that the first hike in the key interest rates took place (for the deposit rate from -0.5% to 0%). In the meantime, the tone has completely changed and the ECB is pointing out the dangers of excessively high and very persistent inflation.

The long-term commitment to an expansionary policy was counterproductive

One reason for the ECB's delayed response to the inflation surge was the so-called "forward guidance," an unconventional tool used by the central bank to anchor expectations in financial markets. In the later part of 2020 and early 2021 markets were expecting policy rates to remain practically at zero until 2024. The design of the forward guidance changed somewhat over time, but it was clear that net bond purchases under the APP would have to end before any rate hike and that inflation would have to be compatible with the price stability objective well within the ECB's projection horizon and also over the medium term. Tying interest rate hikes to the end of net bond purchases under the APP, which was decided to be at the beginning of the third quarter of 2022, proved counterproductive as inflation by then had soared. A timely reaction was made difficult by extensive forward guidance.

.

Consequently, the ECB beginning in August 2022, switched to a meeting-by -meeting (MBM) approach entailing the evaluation of incoming data for policy decisions. This approach grants more flexibility, which is needed in times of extremely high uncertainty and considerable inflation dynamics.

The uncertainties in diagnosing and forecasting economic developments that have always accompanied monetary policy decisions have arguably been somewhat underrated in the model-based paradigms of recent years (not only in EMU). The notion that we live in a world of very low, possibly at times even negative equilibrium interest rates and that central banks can therefore only exert influence via large-scale bond purchases has shaped policy for many years. But there are major uncertainties attaches to such calculations and in today's situation, the thought may lead to quite different conclusions. By and large, the persistent overshooting of inflation above the desired two percent suggests that the current interest rate level has not yet reached the equilibrium interest rate, which is not directly observable. It seems to be much higher than suggested by the earlier model calculations. Any such conclusions are however problematic in an environment of very high uncertainty.

The ECB should pay more attention to changes in the money supply

Stabilizing the price level and macroeconomic developments is a medium-term objective. This has probably been widely accepted since the failed and inflationary attempts at short-term cyclical policies in the 1960s and 1970s. But how can it be implemented? One way, in the years of monetarism, was to assess the contribution of monetary policy to the stability of prices and macroeconomic developments via the evolution of the money supply and credit aggregates, which monetary policy can influence more directly than the ultimate objective of the price level. Over time, the focus on monetary aggregates has fallen out of fashion again, and the ECB has also relativized the importance of monetary developments due to a supposedly looser connection with price level developments in the more recent past.

However, empirical results are always time-dependent. If in the past three to four years attention had been geared a bit more to money growth - M1 growth skyrocketed by around 25% in 2020 and 2021 combined - the normalization of monetary policy would probably have been tackled much earlier and more whole-heartedly. Although many other factors beyond monetary growth played a major role for inflation in the short term, its rise to 8.4% in 2022, which followed the surge in M1, could at least have been slowed. In the meantime, and mainly as a result of the interest rate hikes since mid-2022, the narrow monetary aggregates in the euro area have come back down significantly, which bodes well for an imminent slowdown in inflation.

In retrospect, the huge bond purchases appear questionable

During periods of low inflation, the ECB often pointed to potential problems in transmitting its monetary stimulus to the real economy especially as a result of the effective lower bound for interest rates, which limits its room for maneuver. It therefore launched immense bond-buying programs, removing interest rate risks from the market on a large scale and depressing yields on the capital markets. Government bond prices rose sharply and also pulled up the valuations of asset securities such as equities, shareholdings and real estate.

The extent to which the rise in asset prices stimulated aggregate demand and price developments is debatable, as there were also negative effects. Greater inequality in the distribution of wealth and slower growth in retirement assets may have led to higher saving, dampening expansionary effects of bond purchases.

Regardless of how one views the effects of unconventional policy, what is clear is that we are now witnessing a correction. The reversal of monetary policy has resulted in significant valuation losses. In 2022, both bonds and equities were heavily affected, and while stocks have been recovering in 2023, real estate is undergoing further revaluation. Financing conditions have deteriorated considerably as a result of much stricter lending standards on the part of banks, and corporate loans and housing loans have become markedly more expensive. The euro area economy is stagnating. The adjustments to higher interest rates are ongoing and can be seen as a burden for private households and the corporate sector. Moreover, the central bank itself is affected as the huge stock of bonds it acquired as part of quantitative easing has lost considerable market value. Selling these bonds would turn hidden into realized losses and further increase the rise in yields. Also for these reasons, only a slow reduction in the ECB's bond holdings can be expected.

Inflation expectations are of particular importance for monetary policy

An important prerequisite for the long-term stability of the price level is to anchor economic agents' inflation expectations as firmly as possible at the stability target. The ECB succeeded quite well in this until the current inflation shock. Even in the current situation with very high inflation, financial market participants only foresee inflation of around 2.5% over the next five or ten years, which is at least not very far from the central bank's target.

With regard to private households, however, there are significantly greater inflation concerns and thus deviations from the central bank's stability target. The ECB should and will take this into account in further decisions and continue its stabilization course to normalize household’s inflation expectations.

In this respect, the credibility of the central bank is of central importance. The ECB will now have to prove its continuity and stamina under difficult conditions. A continued exit from years of expansionary policy with increased interest rates and a reduction in large bond holdings will not only put a strain on the central bank's own balance sheet, but will also further slow economic development.

Conclusion

The economic environment has changed quite dramatically since the ECB's 2020/21 strategy review. The sudden spike in inflation has significantly raised perceptions about longer-term inflation trends and the "equilibrium" level of interest rates. The task now is to curb inflation and anchor overly high inflation expectations back near the 2% target.

The costs of fighting inflation are already visible in the form of a stagnating economy and heightened recession concerns. The price is now being paid for the extremely expansionary unconventional measures of the past. The burdens caused by the abrupt turnaround in monetary policy cannot be avoided. However, the more credible and reliable the central bank's actions are, the lower they will be. A consistent and clearly communicated stabilization course, in which the required interest rate level is maintained for a while and the reduction of the bloated balance sheet is tackled, should soon repair the reputational damage brought about by the inflation acceleration and consolidate the ECB's credibility.

Because of the costs of a stabilization policy, there are already calls for the central bank to tolerate higher inflation or to abandon inflation targets altogether. That would be the wrong way to go. Price level stability is a crucial prerequisite for steady growth in the long term.

Why Currency Hedging is Essential When Purchasing Global Bonds

Bonds are the safe harbours within a portfolio, meant to reduce overall risk. However, they do not always live up to this function, as investors experienced particularly during the historically poor investment year of 2022. However, a study by Sebastian Dörr shows that such fluctuations are nothing out of the ordinary in global bond investments without currency hedging.

The capital market analyst from HQ Trust calculated the return and volatility of the Bloomberg Global Aggregate Global Bond Index and compared them with the values of its currency-hedged version: Would bond investors have been able to sleep just as soundly in the period from 1999 to April 2023 without currency hedging? Not really, especially with the fluctuations that Sebastian Dörr calculated using the so-called rolling 12-month volatility, there were considerable differences.

- "Without currency hedging, fixed-income securities sometimes reached volatilities reminiscent of equities. The 'volatility' peaked at more than 11%.“

- "In contrast, the risk with currency hedging usually fluctuated only between 2 and 4%.“

- "The 7% observed over the past 12 months further illustrate the impacts of the strongest interest rate increases in 40 years.“

- "In this context, the fluctuations of the hedged variant also exceeded those of the index variant without hedging for the first time.“

- "Over the period shown, hedging against currency fluctuations would have also paid off in terms of performance: The return was 13% better than the unhedged variant.“

"Chart of the Month” from HQ Trust: Which fund managers beat the index (and which ones don't)

There are numerous analyses that focus on the performance of active fund managers. The results are usually the same: only a few succeed in outperforming the market. However, a study conducted by Florian Ehrlinger reveals that this is not the case for all sectors, highlighting significant differences.

Florian Ehrlinger, the capital market analyst at HQ Trust and co-portfolio manager of "HQT Megatrends," analyzed the post-cost performance of approximately 2,750 actively managed funds over the past 10 years. Ehrlinger categorized the products according to their three investment styles: value, growth, and blend - a category where the fund manager can select stocks from both areas. The analyst compared the fund returns with their respective MSCI indices: the MSCI ACWI Growth, MSCI ACWI Value, and MSCI ACWI.

"Over the past 10 years, fund managers in the growth sector managed to beat their respective benchmark index 6 times."

"On average, the outperformance against the MSCI ACWI Growth during these years amounted to 4.2 percentage points."

"It is worth noting that in all 6 years when growth managers outperformed the benchmark, growth stocks performed better than value stocks."

"In 2020, the year with the highest growth outperformance, value managers had the highest underperformance."

"The performance of the blend category is disappointing, with the average return surpassing the benchmark in only one year. Value managers achieved this feat only 3 times. This demonstrates the critical importance of professional fund selection." "Not surprisingly, product costs have a significant impact on returns. Across all comparison groups, the average cost stands at 0.87%. With lower costs, many managers would achieve better results."

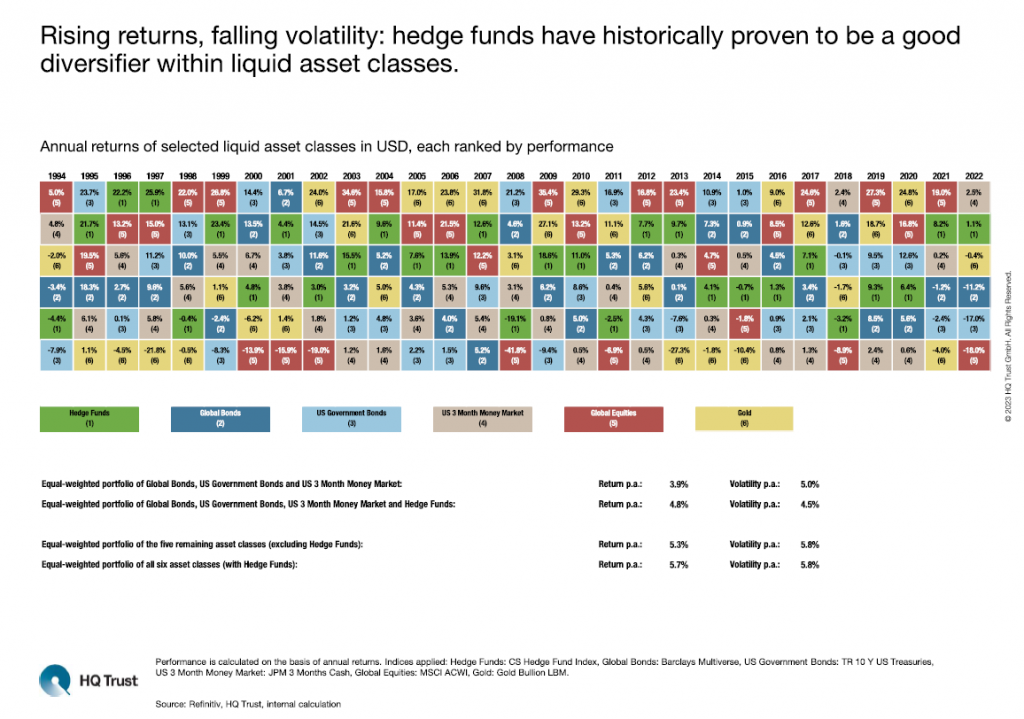

"Chart of the Month” from HQ Trust: How hedge funds affect a portfolio

There is a lot of stock market wisdom about the advantages of a broad diversification of assets. Dr Thomas Neukirch has analysed whether this also applies to hedge funds, which invest in assets such as equities, bonds, credit markets or commodity contracts and pursue very different investment objectives.

The Head of Strategic Asset Allocation and Hedge Funds at HQ Trust calculated how the addition of hedge funds would have affected a portfolio with low volatility asset classes - Global Bonds, US Government Bonds and Money Market. In a second step, Dr Thomas Neukirch added equities and gold. The analysis covers the period from the beginning of 1994 to the end of 2022.

- "Rising returns, falling volatility: hedge funds have historically proven to be a good diversifier in the context of liquid asset classes."

- "Looking at low volatility asset classes, the addition of hedge funds to an equally weighted portfolio of global bonds, US government bonds and money market caused an improvement in volatility and return."

- "Annualised return increased from 3.9% to 4.8% for the hedge fund variant, which was also equally weighted. At the same time, volatility decreased from 5.0% to 4.5%."

- "Looking at a portfolio that included gold and global equities in equal proportions alongside hedge funds, global bonds, US government bonds and money market, the message is similar."

- "Over the long term, this portfolio returned an average of 5.7% p.a. with volatility of 5.8% p.a. Without hedge funds, the portfolio would have returned only 5.3% p.a. with the same volatility risk."

What investors should know about hedge funds:

- "The term hedge fund is a collective term for investment funds that invest in a wide variety of ways in mostly liquid investments such as stocks, bonds, credit markets or commodity contracts."

- "Hedge funds can pursue very different investment objectives: Many funds aim to generate returns independent of the capital markets. Other funds take an activist approach, seeking to generate excess returns over equities with equity market-like risk."

- "At HQ Trust, hedge funds are mainly used as a complement to fixed income investments and for diversification."

- "Hedge funds are therefore particularly interesting for investors who have relatively high bond ratios and are looking for alternatives to them, as well as for investors for whom a reduction in portfolio fluctuations is important."

- "Building a hedge fund portfolio requires many years of experience due to the complexity of the asset class."

"Chart of the Month” from HQ Trust: Infrastructure investments: A very special inflation hedge

Weak economy, high inflation, great uncertainty: Kristina Chorna and Michel Caspary analyze how infrastructure investments have performed in such an environment in the past - and how promising these investments remain.

For their study, the two infrastructure experts from HQ Trust determined the annual demand for infrastructure investments in the various sectors and regions. In addition, Kristina Chorna and Michel Caspary calculated the average return of private infrastructure investments compared to a broad equity index such as the MSCI World and the S&P Infrastructure, which contains 75 stocks from the sector - and analyzed the return in different inflation phases.

Commenting on the annual demand for infrastructure investments, Michel Caspary, investment manager, real estate and infrastructure at HQ Trust, said:

- "Demand for private infrastructure investment remains high: current investment will not meet demand, which is estimated at around USD 3.9 trillion annually through 2040."

- "This compares to just USD 178 billion raised by infrastructure funds in 2022. This represents just 4.6% of global demand."

- "The greatest demand is currently in Asia, but annual demand in the infrastructure markets of Europe and North America is also still well above what is being collected by funds. Among sectors, demand is highest in transportation and energy, followed by telecom and water."

- "Economic downturns or crises do not change the high demand. Since infrastructure provides essential services, usage generally declines only slightly."

On returns, Kristina Chorna, head of infrastructure at HQ Trust, said:

- "Comparison with other investments shows that private infrastructure assets offer attractive and stable returns, even in an inflationary environment."

- "Infrastructure's resilience has been most evident in the past during weaker capital markets. The sector did particularly well during periods of low GDP growth and high inflation."

- "Rising inflation-related costs and interest rates can usually be passed on to customers through contractual agreements, regulation or pricing power."

- "Across all sectors, more than 2/3 of companies are able to do this."

- "HQ Trust's current focus is on investment strategies with a return mix of ongoing revenue secured through long-term contracts and value enhancement measures that come from operational improvements such as revenue growth, cost reduction or buy-and-build strategies."

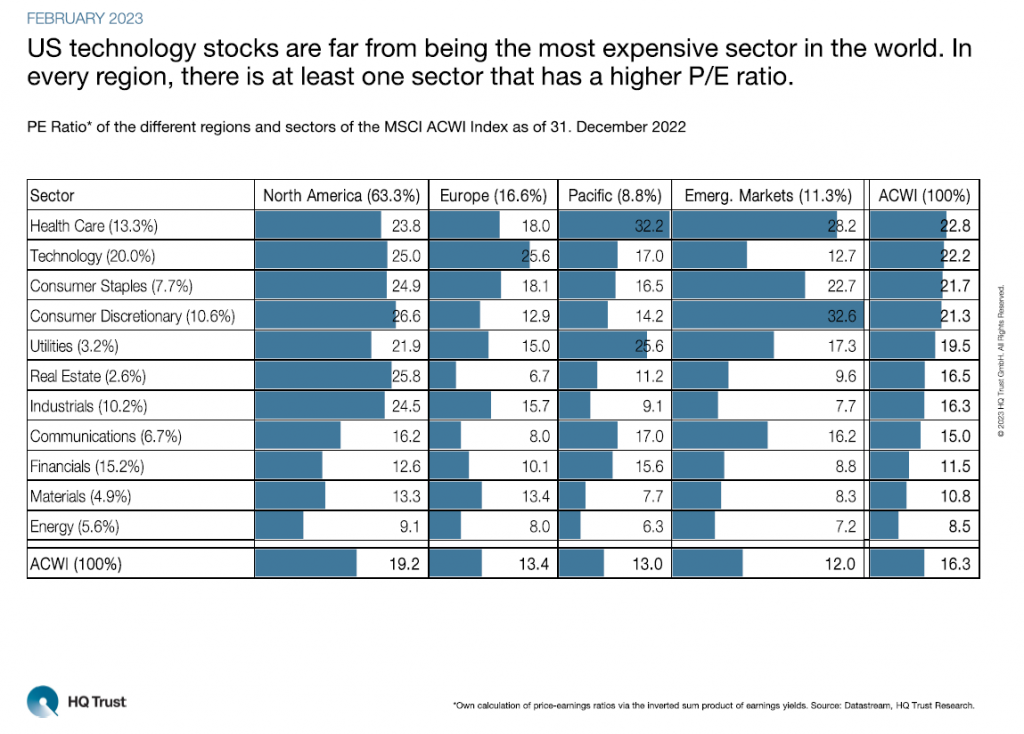

"Chart of the Month” from HQ Trust: The most expensive sector in the world

Let's say you're sitting at “Jeopardy” and are asked the following question. The shares of which region and sector currently have the highest valuation? The choices are: U.S. technology stocks, European industrials, healthcare companies from the Pacific region or cyclical consumer goods manufacturers from the emerging markets. Pascal Kielkopf would have known the answer. Would you?

In his new research, the capital markets analyst at HQ Trust has broken down the MSCI ACWI global equity index into its individual regions and respective sectors and calculated the corresponding price-to-earnings (P/E) ratios at year-end 2022. To do this, he looks at the four major investment regions - North America, Europe, the Pacific and emerging markets - as well as the 11 sectors.

- "U.S. technology stocks are far from the most expensive sector in the world. In every region, there is at least one sector that has a higher P/E ratio."

- "Of the three most highly valued sectors in the world, none currently come from North America: consumer cyclicals from emerging markets, followed by healthcare companies from the Pacific Rim and emerging markets are all more expensive."

- "Although stocks from North America are currently priced significantly higher than the other regions, with a P/E of 19.2, they come in at the highest P/E in only 4 of 11 sectors."

Pascal Kielkopf's detailed view shows how important it is to also look at the exact background in such an analysis:

- "Investors should not only look at country or sector P/E ratios, but pay attention to how the results came about."

- "For example, individual stocks in certain regional sectors have enormous weight. Australia's Woodside Energy, for example, alone accounts for nearly half (43.5%) of Pacific energy companies."

- "Accordingly, there are often only a few companies that determine the sector's valuation."

- "In what is currently the world's most expensive regional sector - emerging market cyclical consumer goods manufacturers - the 3 Chinese online retailers Alibaba, Meituan and JD are almost exclusively responsible for the extraordinarily high valuation."

- "Calling US techs the most expensive sector would not be entirely wrong about the ACWI. Due to their high weight, they pull up index valuation the most."

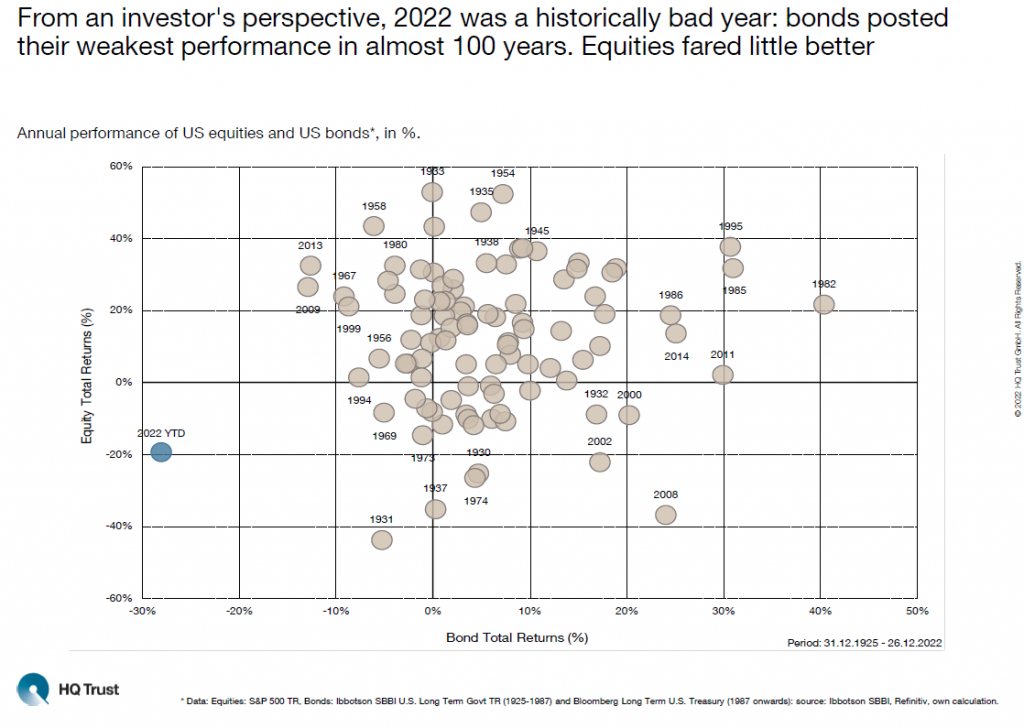

"Chart of the Month” from HQ Trust: A historically bad investment year

There are many reasons for the poor performance of stocks and bonds in 2022: Ukraine war, pandemic, inflation, energy crisis. However, a comparison by Sebastian Dörr shows that it was even a historically bad year from an investor's point of view.

The capital market analyst at HQ Trust compared the performance of U.S. stocks and bonds with that of previous years. How often were the asset classes in positive territory, and how often did they end the year in negative territory? Sebastian Dörr's analysis covers the years from 1926 to 2022.

- "From an investor's perspective, 2022 was a historically bad year. Bonds posted the weakest performance of the past 97 years. Equities didn't look much better."

- "Since 1926, there have been just six years when stocks fell more than they have in the past 12 months: 1930, 1931, 1937, 1974, 2002, and 2008."

- "Years in which stocks and bonds have negative performance have been extremely rare in the past: Since 1926, this has been the case only 7 times."

- "In more than half the cases, stocks and bonds ended the year with a gain: in 51 of 97 years."

- "In 20 years, only stocks gained; in 19 years, only bonds gained."